TLDR: Agentic commerce doesn’t create new taxes—it creates new ways to trigger old ones without leaving a clear record. The problems are attribution, stacked instruments, cross-border VAT, and what governments do when the money flows grow large enough to notice.

Read earlier pieces: Part 1 • Part 2 • Part 3 • Part 4 • Part 5 • Part 6 • Part 7

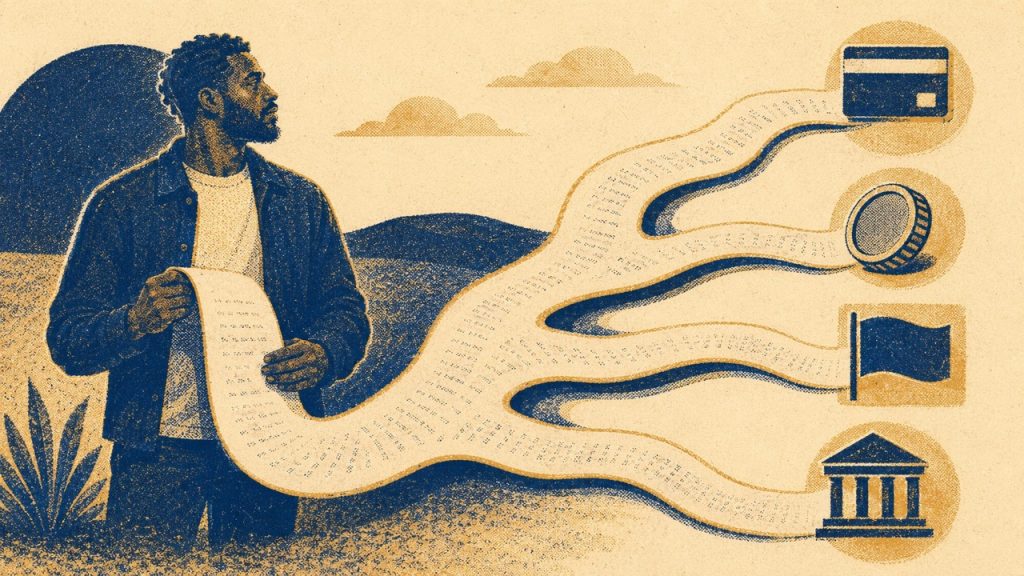

Over one month, a household shopping agent runs 47 transactions across six merchants, three countries, and two cards.

One card belongs to the person. The other belongs to their company and gets used for home-office supplies.

In one checkout on the company card, the agent stacks a Nectar redemption, a cashback credit, and a discount code because, from its point of view, that creates the lowest price.

The agent follows the instruction and saves money.

Then January arrives, the user opens their self-assessment, and the purchase trail looks less tidy.

Some purchases were personal, others were business. Some used personal rewards on a company card, and a few purchases crossed borders.

Some discounts reduced the price, and some rewards may need different treatment.

That’s the tax problem in agentic commerce.

There are no new taxes here, just new and faster ways to trigger old ones.

Under current UK and US law, the tax consequences of an agent’s purchases still follow the person or company behind the agent. The agent doesn’t become the taxpayer.

The law looks through the software and asks who owned the money, who gave the authority, and who received the benefit.

So the first problem isn’t who the taxman sees; it’s the record.

A human buyer leaves a receipt, card statement, maybe an invoice.

An AI shopping agent leaves a transaction log, and that log may or may not contain the information a person, accountant, merchant, or tax authority needs later.

Three problems follow from this:

- Agents blur personal and business spending inside the same basket.

- Agents move across merchants, cards, loyalty systems, and borders faster than the tax record can explain.

- Once the money flow grows large enough, governments will look for a new place to collect.

Who does the taxman see?

The first tax question is attribution: whose money, and whose decision?

Current law provides some answers.

In the US, AI agents aren’t separate taxpayers. The IRS has issued no guidance for autonomous agent transactions, so liability still falls on the person or entity whose assets and authority the agent used, under the general income rules in IRC §61.

In the UK, HMRC’s VAT framework already recognises principal and agent relationships as separate parties. Where a genuine agency relationship exists, the principal carries the underlying supply obligation.

But HMRC hasn’t yet applied that framework to AI shopping agents, and there’s no income-tax ruling that explains how attribution works when an autonomous agent buys on behalf of a person or company.

So attribution may be the easier part. The harder part is evidence.

A VAT-registered business in the UK must keep digital records under Making Tax Digital. That framework already covers orders, delivery notes, purchase invoices, and electronically structured transaction data.

So, in theory, agentic commerce can fit. A merchant with an automated checkout system can create the right record without a human touching it.

But there’s a catch. The obligation sits with the VAT-registered business, and HMRC says purchases made through a third-party agent don’t fall within the digital record-keeping rules until the information reaches the principal.

That’s where the problem starts.

The protocol log may exist. The merchant may have generated a compliant invoice, and the payment provider may have a full event trail.

But unless the agent hands the right record back to the buyer, the buyer may still end up with a pile of transactions rather than a tax-ready record.

The duty bites at the handover.

Whatever the agent did, the user still needs a record they can use when tax season comes.

The stacked-instrument problem in agentic commerce

The second problem is the way agents combine payment methods, rewards, and discounts.

A human may pause before using a personal loyalty account on a company card. An agent optimising for the lowest net price may not pause at all.

In the UK, HMRC’s treatment of rewards turns on the context. Cashback received in the course of trading can be a taxable receipt of the trade.

Personal cashback is generally outside capital gains tax because HMRC says it is not a capital sum derived from an asset, though HMRC also notes it may be income if received through a business or employment.

For an ordinary private customer choosing one retailer over another, HMRC’s position under Statement of Practice 4/97 is that the customer isn’t providing a recognisable service, so the cashback falls outside miscellaneous income.

But the agent doesn’t know which side of the rule it is on.

It sees a basket, price, reward balance, discount code, and payment method. It may fold a personal loyalty redemption into a company-card checkout whenever that produces the lowest number.

Unless the agent has been told not to, it has no reason to treat that as a tax-sensitive choice.

So the Nectar redemption on the company card could become a business record problem. The agent doesn’t flag it, and the user may not see it.

The accountant may not find it unless the raw log separates the payment card, the loyalty account, the redemption, the discount, and the purpose of the purchase.

The US has a similar split. Under IRS Revenue Ruling 76-96, rewards earned through spending are usually treated as a rebate.

IRS guidance on purchase-price adjustments also treats certain rebates as reductions in purchase price rather than income, which is why rewards can reduce the purchase price rather than create income (though this ruling looks disputed).

But business-card rewards still affect bookkeeping.

Cashback tied to business spending can reduce the deductible expense, which creates the same problem in another form: the agent may get the cheapest outcome while leaving the records in a state the business cannot easily explain.

The rule may not be new, but the agent creates more chances to trip it.

The tax jurisdiction problem in agentic commerce

A single agent session can touch several tax systems at once.

Let’s start with VAT.

Under HMRC’s marketplace framework, a platform that sets the terms, handles payment, and arranges delivery may become the deemed supplier and account for the VAT.

That works well enough when a person buys from one marketplace.

But an agent may search several platforms, split a basket, compare sellers, route payment through a wallet, use loyalty points from one system, and deliver goods from several jurisdictions.

The question then becomes which platform owns the VAT on which part of the purchase.

The current system is already strained. Amazon has proposed extending deemed-reseller rules to all marketplace sales, citing analysis it commissioned that puts annual sales by VAT-avoiding bad actors across UK marketplaces at up to £3.2 billion.

Then there’s ‘permanent establishment.’

In broad terms, a business creates a permanent establishment in a country when it has a fixed place of business at its disposal, in a set location, with some permanence, through which the business is carried on.

Agentic commerce doesn’t fit neatly into that picture.

An AI shopping agent has no legal personhood or residence. But a deployer may have systems, infrastructure, staff, customers, payments, and transaction flows spread across several countries.

If the agent habitually concludes contracts in a market, there’ll be questions about whether existing treaty rules can reach that activity through the deployer’s own footprint or through dependent-agent analysis.

Tax scholars have started asking that question, with one arguing that current treaty rules can’t easily assign taxing rights to something that has no legal personhood or place of residence, and that this is becoming a frontier question for AI tax policy.

There’s a similar problem in the US at state level. Economic-nexus thresholds were drawn for sellers, not autonomous buyers. And the consumer-protection rules for electronic transfers give no clear framework for agentic purchases.

So the problem isn’t that every agent purchase creates a cross-border tax issue. Most will not.

The problem is agentic commerce increases the number of sessions where personal, business, platform, merchant, payment, loyalty, and jurisdictional records sit in different places.

And no tax authority has yet given agentic-commerce-specific guidance for that kind of edge case.

What AI shopping agents do to the tax base

The first part of the tax problem is compliance. The second part is the size of the pot.

Governments tend to take action when a large flow of money becomes visible, concentrated, and hard to tax through the old corporate-tax route.

That’s one reason digital services taxes appeared.

Several governments watched major platforms book large advertising revenues from local users while profits moved through low-tax structures, then created taxes that reached revenue rather than profit.

France enacted a 3% levy in 2019 on qualifying digital revenues generated from French users. The UK introduced its own 2% rate from April 2020.

Both taxes sit beside a large flow of money and take a cut from qualifying digital services.

That model is relevant to agentic commerce because agentic transactions may also collect around a few platforms, protocols, payment rails, and cloud providers.

Gartner projects 90% of B2B buying will run through AI agents by 2028, routing over $15 trillion through agent exchanges.

It’s a projection, not a settled future, but the direction is relevant. A large transaction flow, routed through a small number of collection points, invites tax design.

There are already early proposals pointing in that direction. One academic paper sketches a per-token levy collected by cloud compute providers acting as intermediaries between model developers and governments.

That’s not an agentic commerce tax, but it shows the same policy instinct: find the infrastructure layer, then collect there.

Meta’s digital-services-tax handling shows how quickly that can reach the layer below. Meta has started passing DST costs on to advertisers as explicit location fees from 01 July 2026.

So even when a tax targets platforms, the cost can move into the invoices of the businesses and customers beneath them.

Agentic commerce gives governments a similar target: a large automated transaction flow, tied to platforms and protocols, with records that already need to be machine-readable.

The label may say automation, compute, marketplace, payment, or agent transaction. But the logic will look familiar: a large flow, a collection point, and a government looking for its share.

Where this leaves agentic commerce tax

The tax problem in agentic commerce is not that agents create a new taxpayer. The evidence suggests they don’t.

The taxman today still looks through the agent to the person or company behind it.

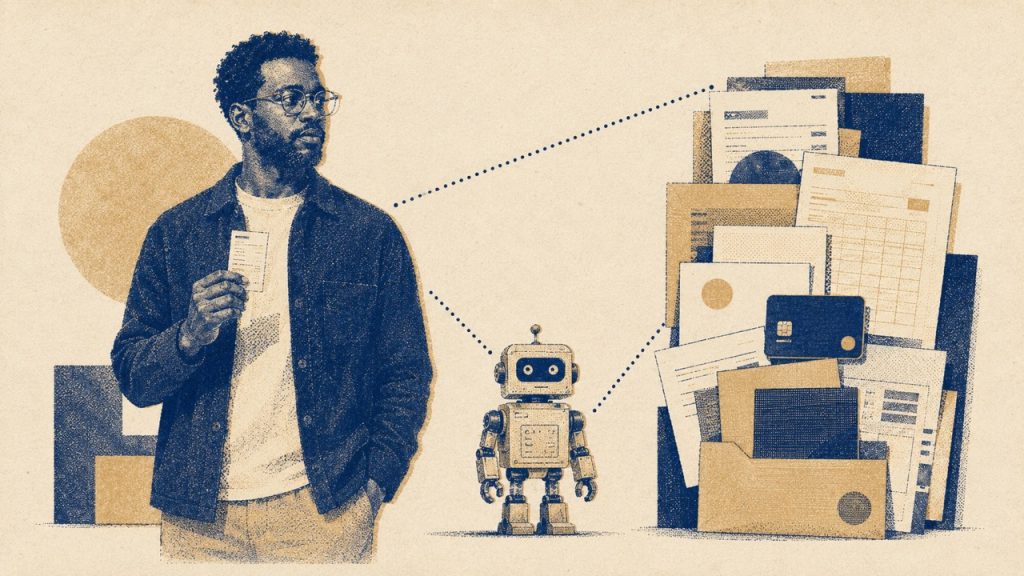

The problem is agents create a new kind of evidence trail. They move across cards, merchants, discounts, points, wallets, and borders faster than ordinary receipts can explain.

And unless the agent hands back a tax-ready record, the user has to reconstruct intent after the money has moved.

That record needs to show what was bought, who paid, which entity benefited, which rewards were used, which discounts applied, which merchant supplied the item, which platform handled the checkout, and which jurisdiction touched the purchase.

Some of that already exists in payment logs, merchant systems, and the agent’s own trace. But tax systems need the pieces brought together at the handover.

That’s where agentic commerce tooling has to go.

Not only payment, authority, and dispute logs, but records a human, accountant, merchant, and tax authority can read when January (or April) arrives.

Disclaimer: Nothing in this article constitutes tax, legal, or financial advice. The analysis is provided for informational and educational purposes only and reflects the author’s own research and thinking. Tax rules vary by jurisdiction and individual circumstance. If you have questions about your own tax position, consult a qualified tax adviser or accountant.